Image: Dreamstime

The virus’s second wave is impacting order books and H1 2021 will be a pivotal period for many contractors, says Kris Hudson

Q3 2020 saw some encouraging improvements in the economy. UK GDP increased 15.5% quarter-on-quarter, and construction output rose by 41.9%. Yet this strong growth came before the second wave of lockdown restrictions were imposed and remains 8.2% below pre-covid levels.

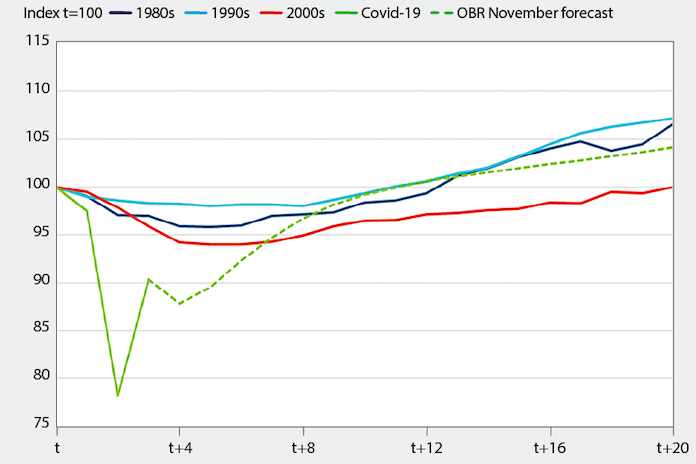

While the vaccine rollout is coming into view, the impact of the pandemic on the economy cannot be underestimated. The recession we saw during H1 2020 may have been short-lived, but it was significant. The impact is stark when you compare the economic hit to previous recessionary periods.

The Office for Budget Responsibility (OBR) November forecast suggests it will be 2022 before we return to the peak seen before the recession. The hope is that a vaccine programme can improve that position before we get the OBR’s next forecast and the Budget in March.

UK GDP performance during recessions

Time period: t = quarter prior to first quarter of GDP contraction, t+20 = 20 quarters after GDP contraction. Source: ONS & Office for Budgetary Responsibility

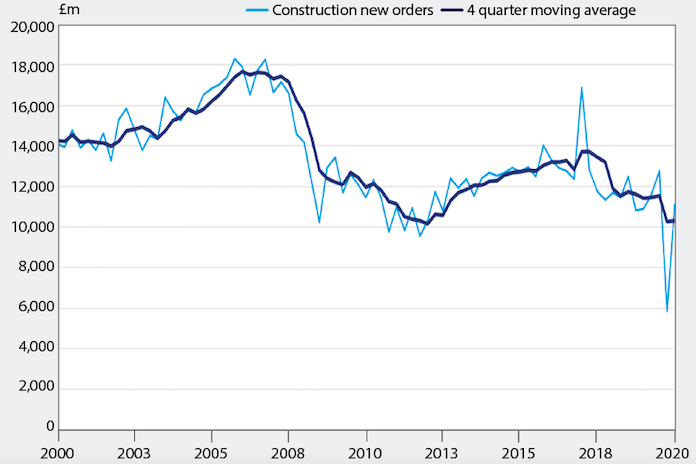

It’s a similar story for construction. On the surface, we’ve seen huge improvements during Q3 2020. Housing output rose 84.4% on a quarterly basis, and new orders in infrastructure jumped 108.2% in the same period. But these figures mask the deeper covid impact.

Looking at the longer-term trend, new orders for construction are weakening. The pipeline of work in the industry is considerably below what it once was. The Q3 bounce, while welcome, is only the start and puts into stark perspective how much further we have to go given new orders are some £4bn down, in nominal terms, on the same point 20 years ago.

Construction new orders performance

Source: Office for National Statistics (ONS)

With the second wave of the virus likely to impact order books and output in Q4 2020 and Q1 2021, workloads may be constrained further before they strengthen.

The first half of 2021 is going to be a pivotal period for many contractors, and it will be vital to stay alert to the risk of insolvencies and the resilience of the supply chain. Particularly given the potential for commercial pressures after Brexit, due to the risk of materials delays and restrictions to the free movement of labour.

With the government leading a ‘build back better’, levelling-up approach to recovery, and a National Infrastructure Strategy finally unveiled, the industry will need to reorganise to ensure that the capacity is in place to meet future demand.

Kris Hudson is an economist and associate director at Turner & Townsend