As the reopening of construction gathers pace, Kris Hudson examines where construction output goes from here and why collaboration will be key to the sector’s survival.

With the accelerating reopening of construction sites and suppliers, June saw the fastest rise in construction activity for nearly two years, according to the latest IHS Markit / CIPS UK Construction Purchasing Managers’ Index (PMI). After three months of steep falls, new orders also stabilised, giving the indication that the industry was finally reaching a stronger footing – albeit still shakier than many had initially speculated.

We are certainly not out of the woods yet though. The Office for Budget Responsibility (OBR) has revised its UK GDP forecast and now expects a contraction of -12.4% in 2020. That represents the worst economic performance in 300 years. If that rings true, the longer-term impact on the construction industry, and in particular pricing, may be considerable.

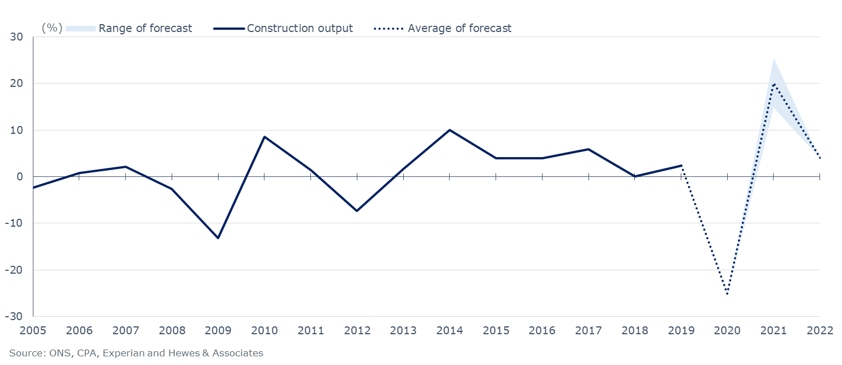

As a rule of thumb, construction output follows the directional changes of GDP, but its movements are more amplified. The Construction Products Association (CPA) finds that construction output can be three times more volatile. Construction is investment led and predominantly private sector driven – confidence is key and any changes in sentiment can affect business decision-making.

Therefore, while the average forecast of construction output suggests a -25% fall this year, if we see a double-digit drop in GDP, a further reduction to output is not beyond the realms of possibility.

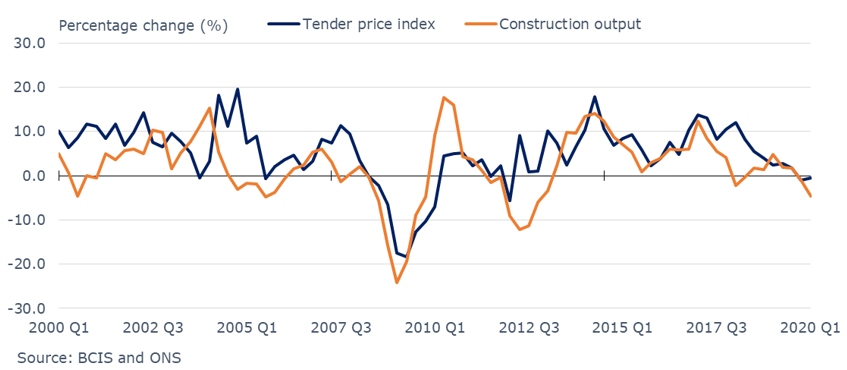

This is important because output also has a strong, positive correlation with pricing. Our analysis shows that just over a third of the variation in tender price inflation is driven by movements in construction output.

Collaborate to survive

Decreased market activity typically leads to a more competitively priced market – and even deflation – as delivered output drops and investor confidence wanes. Contractors can become less selective over tendering opportunities and reduce prices, despite the risks.

The government’s infrastructure-led recovery may support price stability to an extent but a simultaneous pickup in private sector demand will be needed to avoid deflation. In the absence of this, deflationary pricing and supplier insolvencies are likely to follow.

Against such a turbulent economic environment, we need to preserve the capability that sits within our industry. Transactions looking to exploit cost reduction opportunities will only hinder our supply chain in the medium to long term, ultimately driving prices higher for all.

This recession will affect suppliers, consultants, contractors and sub-contractors alike – and it will take close collaboration to weather the storm.

Kris Hudson is associate director at Turner & Townsend

Comments

Comments are closed.

Kris,

I totally agree with your comments, if we are not careful the market will simply drive itself towards low cost, poor productivity, poor quality and conflict. Which in turn will deter clients from investing, invite contractual conflict, cause payments issues and ultimately result in further business failures. I fear for the commercial fit out sector whos clients are still determining how they will move forward in the new normal.

Kris

Like Paul I totally agree with your comments. There are several companies out there who are submitting “suicide” prices already. It is imperative that prices are not “driven to the bottom” but are stabilised to ensure high quality is maintained. Whilst I understand the feeling of “just needing the work” I want our company and others to be here next year and for many years to come – so my advice would be to price accurately and fairly and not to become “Busy fools” by undercutting others prices.

Lara Ayris 13th August 2020